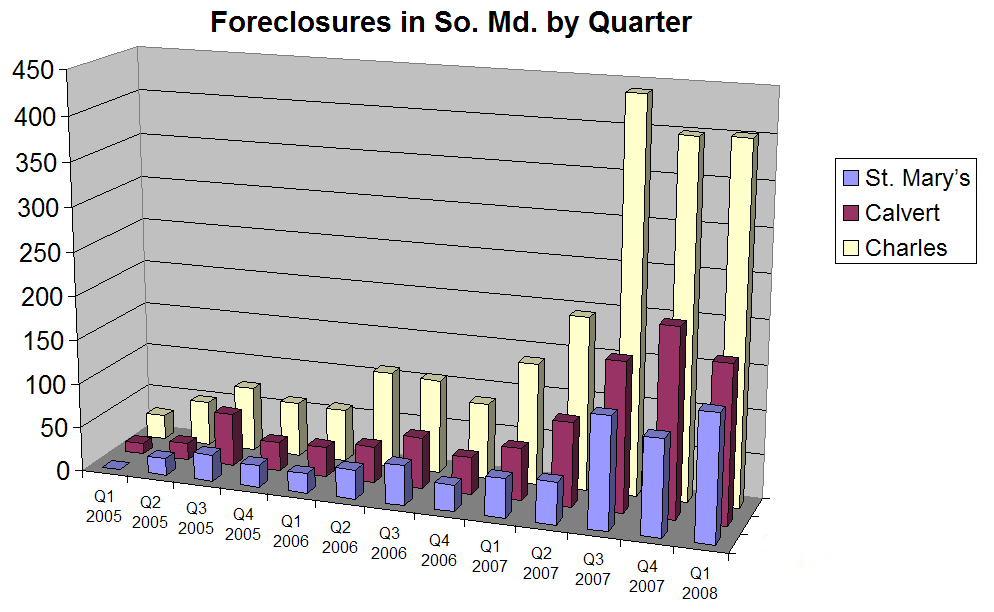

Number of foreclosures in the tri-county area by quarter since 2005. The figures are from RealtyTrac, chart prepared by somd.com. (Click to enlarge chart)

ANNAPOLIS (May 01, 2008) - Many people who found themselves in financial trouble, especially at the time of a major bankruptcy law change passed by Congress in 2005, rushed to file thinking it would save their homes.

Instead, experts say, the ensuing credit damage left many homeowners unable to refinance adjustable-rate mortgages and may have driven them into foreclosure, aggravating the lending crisis that has severely damaged the economy in Maryland and around the country.

Homeowners with bankruptcy on their credit histories were trapped with no way to refinance when their adjustable-rate mortgages reset and they were expected to make higher payments, said Clarence Snuggs, deputy secretary of the Department of Housing and Community Development.

Had they avoided bankruptcy, however, many homeowners might have been able to restructure their mortgages into manageable payments and kept their homes without doing such extensive damage to their credit histories.

Many of the people who fell into this trap were those who had exhausted all other avenues of settling their debt, said Brett Weiss, a Maryland bankruptcy attorney.

The number of bankruptcy filings skyrocketed in October 2005 just before the Bankruptcy Abuse Prevention and Consumer Protection Act went into effect, ostensibly to make it more difficult for irresponsible borrowers to get a free pass on debt.

But the law also hit legitimate filers and meant many were unable to declare bankruptcy at all. Others had to pay back more of their original debt and faced higher filing fees than they would have faced under the previous law, said Anne Balcer Norton, director of foreclosure prevention for St. Ambrose Housing Aid Center in Baltimore.

The bankruptcies affected included Chapter 7 and Chapter 13, the versions that apply to individuals as opposed to businesses.

"Everyone who even had a thought of filing filed before October 2005," Weiss said.

The number of filings in October 2005 was 11,219, almost as high as the totals for the previous four Octobers combined.

The figure plummeted in the following months to less than 3 percent of that and still remains lower than it was in the months before the new law.

Last year saw only 13,131 personal bankruptcies in Maryland, less than half the annual average since 1994.

But as the economy has worsened the number has been rising slowly, and in 2007 foreclosures in Maryland began rising with it.

In the first quarter of 2007 the number of foreclosures in Maryland nearly doubled over the same period of the previous year from 1,081 to 2,031. By the end of 2007, the state saw more than 25,000 foreclosures, 5.5 times the figure from 2006.

Many people suddenly found themselves facing unmanageable payments because of a death or illness in the family, while others had adjustable rate mortgages with payments that increased to more than the homeowners could afford, said Donna Edwards, the Democratic nominee for Maryland's 4th Congressional District seat.

Because of the impact damaged credit can have on a homeowner's ability to restructure mortgage payments, the more recent increase in the number of bankruptcy filings can be taken as an indication of the number of foreclosures that can be expected down the road, said Peter Morici, professor of international business at the University of Maryland.

These individuals need temporary support to help them make new payment arrangements and stay in their homes, Snuggs said.

"People needed to be able to buy some time to restructure that loan with their servicer or refinance into something that would be sustainable for them," Snuggs said.

His department is among those offering help to homeowners who find themselves having trouble with their monthly payments. But in order to do that, he said, those offices need to know there is a problem and many people simply do not make the first move.

There is no blanket advice when it comes to filing for bankruptcy and anyone considering it should seek professional advice before making a move, Norton said. Not only does every situation differ, there are nuances to the law that make it dangerous for an individual to move into bankruptcy without professional help.

"Some people have the impression that bankruptcy is going to resolve everything," she said. In reality, it can let individuals restructure payments on certain properties, including luxury items like boats, but judges have no power to help them keep their primary homes, she said.

The new law not only makes it more difficult for homeowners to file and leaves fewer eligible, she said, but also makes it a bit more expensive, the last thing people in financial trouble need.

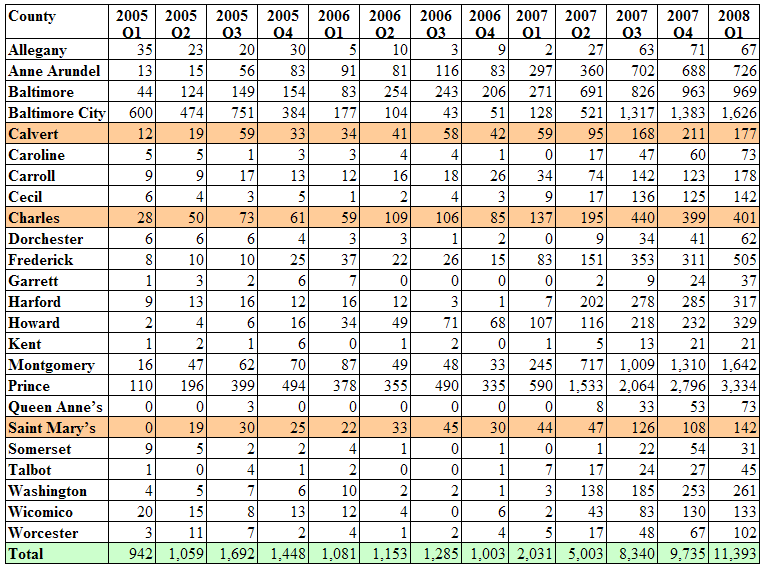

Foreclosure Numbers in Maryland By County, By Quarter

(Click to enlarge chart)

Table shows the number of home foreclosures in each of Maryland’s 23 counties and Baltimore City from the beginning of 2005. The data includes only Chapter 7 and Chapter 13 bankruptcies, the types filed by individuals. The figures are from RealtyTrac, which collects foreclosure data across the United States.

Capital News Service contributed to this report.